Government aid is helping many struggling homeowners stay in their homes, but what happens when foreclosure moratoriums expire?

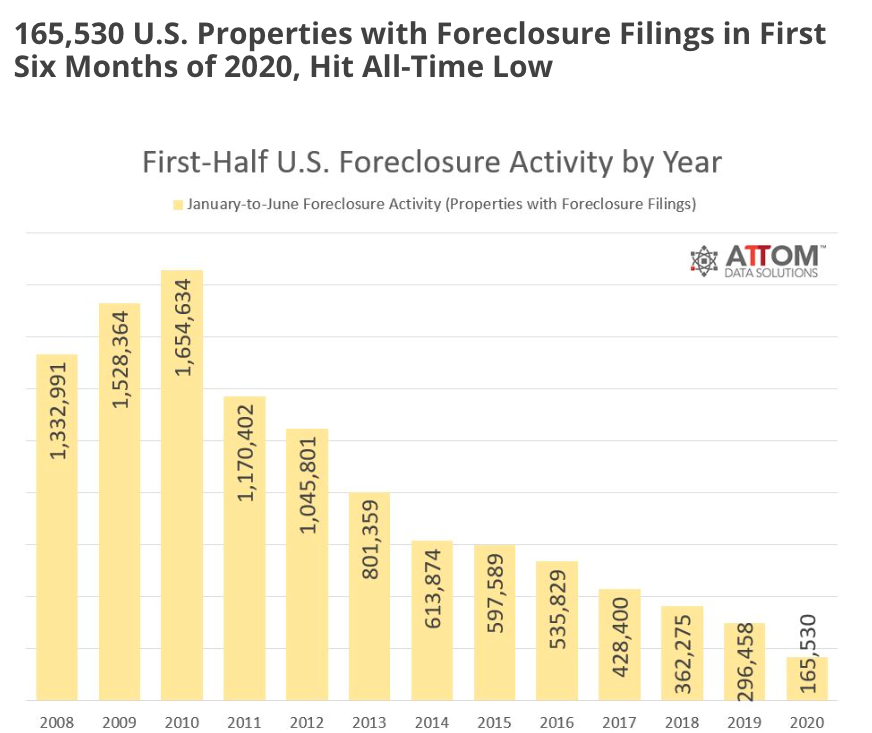

Foreclosure filings—including default notices, scheduled auctions, or bank repossessions—dropped 44% in the first six months of 2020 from the same time period a year ago. They are also at a record low, despite the global pandemic and skyrocketing unemployment, ATTOM Data Solutions reports in its Midyear 2020 U.S. Foreclosure Market Report.

A total of 165,530 U.S. properties received a foreclosure filing in the first six months of this year.

But some economists question whether it’s the calm before the storm.

For now, “the residential foreclosure market across the nation continues to contract amid a combination of booming housing market conditions before the current coronavirus pandemic hit and a moratorium on activity while the country struggles to overcome the crisis,” says Ohan Antebian, general manager of RealtyTrac, a parent company to ATTOM Data Solutions. “Foreclosure starts and completions were already declining rapidly last year because the housing market and economy were riding so high. Now they’re down to lows not seen for at least 15 years as the federal government has banned lenders from pursuing most delinquent loans until at least the end of August 2020 to help people weather the pandemic.”

Once the moratorium is lifted, the distressed property volume is likely to increase significantly. Millions of Americans missed their mortgage payments in June due to unemployment, Antebian notes.

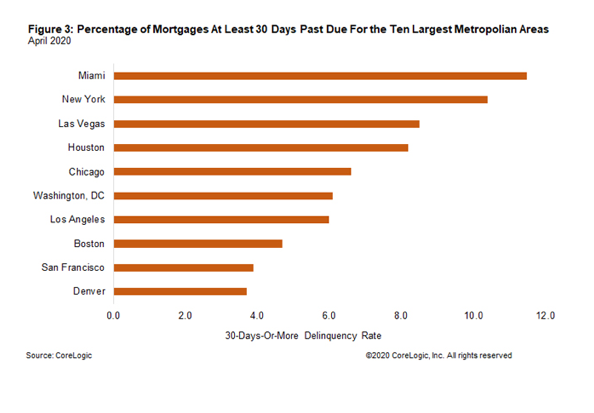

Mortgage delinquencies in April (30 days or more past due) were highest in New York, New Jersey, Florida, and Nevada, according to a separate report, CoreLogic Loan Performance Insights.

Still, while mortgage delinquencies remain high, foreclosures—for now—are tough to find. “For now, everything is on hold and the foreclosure numbers reflect that pause,” Antebian adds.

What happens once the government’s stimulus support ends and foreclosure moratoriums are lifted? Lawrence Yun, chief economist of the National Association of REALTORS®, poses several questions whose answers will depend on what happens next: Will most jobs have come back by then, and hence most homeowners be able to make mortgage payments? Are there sufficient buyers to quickly absorb new foreclosures since the mortgage rates are at record lows?

“These are some of the unknowns,” Yun told Motley Fool’s Millionacres. “My guess is that home prices will still hold on reasonably well due to the known facts: There has been great underproduction of homes over the recent years, and we don’t have funny subprime mortgages that have overstretched consumer budgets.”

Source: “165,530 U.S. Properties With Foreclosure Filings in First Six Months of 2020, Hit All-Time Low,” ATTOM Data Solutions (July 16, 2020) and “Jump in Early-Stage Delinquencies Leads to Highest Overall Delinquency Rate in Over Four Years,” CoreLogic Insights Blog (July 14, 2020)